The AI Executive Brief: January 2026

What Big Consulting Is Saying

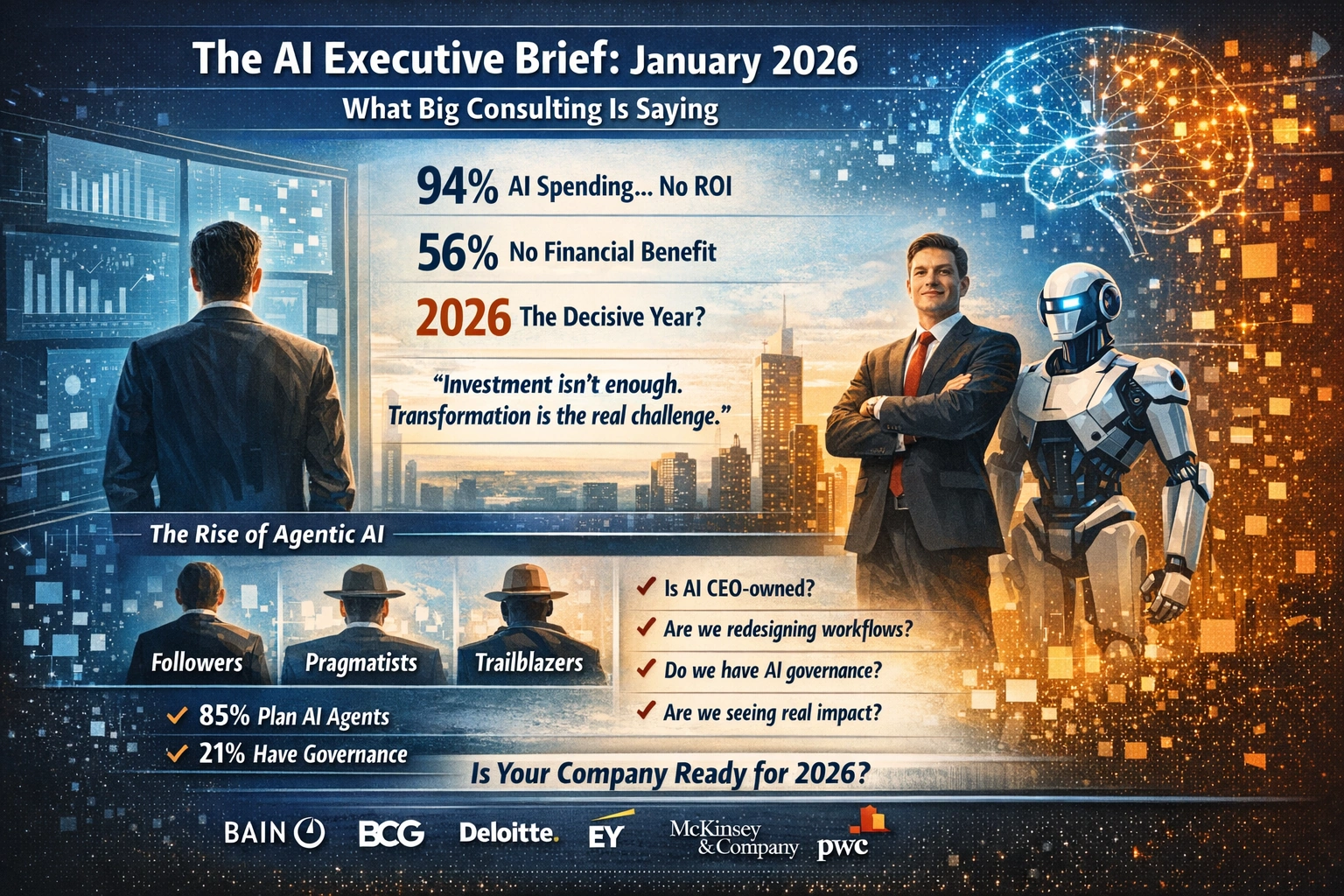

Companies are doubling AI investment. 94% will keep spending even without ROI. Yet 56% of CEOs report no significant financial benefit. Every major consulting firm agrees 2026 is the decisive year — but the data reveals a widening gap between those who transform and those who merely invest.

This brief synthesizes what Bain, BCG, Deloitte, EY, McKinsey, and PwC are telling their clients in January 2026. The message is remarkably consistent: the window between AI leaders and laggards is closing, and the differentiator isn’t spending — it’s organizational transformation.

The Investment Paradox

AI spending is accelerating at an unprecedented pace. BCG reports that corporate AI investment will double in 2026, reaching approximately 1.7% of revenues — more than twice the 2025 level.1 Even more striking: 94% of companies plan to continue investing in AI even if it doesn’t drive immediate returns.1

Yet the returns remain stubbornly elusive for most.

PwC’s 2026 Global CEO Survey puts the gap in stark terms: only one-in-eight CEOs have achieved both cost and revenue benefits from AI, while a majority report no significant financial impact at all.2

Deloitte’s State of AI report confirms the pattern: only 34% of companies report using AI to “deeply transform” their business, while 37% admit they’re using AI only at a surface level with little or no change to underlying processes.3

“AI is delivering productivity for most, but business reimagination for few.”

— Deloitte, State of AI in the Enterprise 2026

The CEO Awakening

If there’s one clear shift in 2026, it’s this: CEOs are no longer delegating AI to IT. They’re taking personal ownership.

BCG’s latest survey reveals that 72% of CEOs now say they are the main decision-makers on AI — twice the share from last year.1 Half believe their job depends on getting AI right.1

This isn’t passive sponsorship. BCG reports that trailblazing CEOs are now spending more than eight hours per week on their own AI upskilling, while investing twice as much as their counterparts in workforce capability-building.1

“We’re seeing a real step up in engagement and ownership around AI by boards and C-suite teams. They’re starting to own end-to-end outcomes rather than delegating experiments and individual use cases.”

— McKinsey, AI’s Next Act

McKinsey’s Kate Smaje emphasizes that 2026 is when executives must convert last year’s prototypes into production systems — with the “humanware” (talent and change management) layered on top that makes impact material and repeatable.4

- Followers (~15%) — recognize AI’s potential but lack full conviction; making cautious investments

- Pragmatists (~70%) — excited and confident, but invest only when they see evident value and low risk

- Trailblazers (~15%) — drive transformation through decisive investment, rapid upskilling, and strong belief in AI’s ROI

Notably, 60% of Trailblazer CEO budgets are allocated to workforce upskilling — compared to 27% for Pragmatists and 24% for Followers.1 The leaders aren’t just buying technology; they’re building capability.

2026: The Year of Reckoning

Every major firm positions 2026 as a pivotal transition — from experimentation to enterprise scaling. The language is remarkably aligned:

| Firm | The Message |

|---|---|

| Deloitte | “From Ambition to Activation” |

| McKinsey | “AI that chats to AI that settles” |

| PwC | “A decisive year for AI” |

| BCG | CEOs “rolling up sleeves” |

| EY | “Tipping point from pilot to enterprise scale” |

Deloitte reports that workforce access to sanctioned AI tools has grown by 50% in just one year — from fewer than 40% to around 60% of workers now equipped.3 But access isn’t outcomes.

The Pilot-to-Production Gap

Only 25% of organizations have moved 40% or more of their AI pilots into production. However, 54% expect to reach that level within three to six months.3 The question is whether that optimism is warranted.

McKinsey offers a sobering prediction:

“In 2026, many enterprises will realise that while AI technology is advancing fast, significant value won’t materialise without the fundamentals — modern IT architecture, high-quality data, capabilities, operating model, and change management. We’ll see a tougher ‘audit moment’ where programmes fall short not because the models underperform, but because the enablers and economics weren’t in place.”

— McKinsey, AI’s Next Act

The Rise of Agentic AI

The most significant shift in the 2026 discourse is the move from generative AI to agentic AI — autonomous systems that don’t just generate content but complete tasks end-to-end.

CEOs have already committed more than 30% of their organization’s 2026 AI investment to agentic AI.1 90% believe AI agents will produce measurable returns this year.1

But McKinsey counsels against over-ambition:

“Everyone expects 2026 to be the year of fully autonomous agents; what is more likely is it’s the year autonomy shrinks by design. Enterprises will move from ‘AI that chats’ to ‘AI that settles’, closing tickets and clearing exceptions end-to-end with audit trails.”

— McKinsey, AI’s Next Act

The real productivity lift, they argue, will come from automating coordination — handoffs, approvals, escalation — not just tasks.4

Bain offers concrete evidence from retail: applying AI solutions to merchandising workflows has created efficiency gains of 50% to 70% for key tasks when paired with AI literacy and redesigned processes.5

The Governance Gap

Here’s the danger signal buried in the data: 85% of companies plan to deploy autonomous AI agents, but only 21% have mature governance models to manage them.3

This is the setup for the next wave of AI failures. Companies are racing to deploy agents without the infrastructure to control them.

“For Agentic AI, governance and growth go hand in hand. Companies seeing the most success are taking a measured approach — starting with lower-risk use cases, building governance capabilities, and scaling deliberately. In the AI era, governance is more than guardrails — it’s the catalyst for responsible growth.”

— Deloitte, State of AI 2026

McKinsey predicts this will be the year of “tackling the foundational enablers required to build, govern, and operate agentic workflows in a way that meets business needs, security obligations and regulatory requirements.”4 Key topics will include at-scale evaluations, agentic observability, and identity and access management for agents.

What Separates Leaders from Laggards

The consulting firms are remarkably aligned on what differentiates the companies seeing real returns:

1. Strong Foundations (The 3x Advantage)

PwC’s analysis is unambiguous: CEOs whose organizations have established strong AI foundations — Responsible AI frameworks and technology environments that enable enterprise-wide integration — are three times more likely to report meaningful financial returns.2

Companies applying AI broadly to products, services, and customer experiences achieved nearly four percentage points higher profit margins than those that did not.2

2. Process Redesign, Not Just Tool Deployment

Only 30% of organizations are redesigning key processes around AI.3 The rest are bolting AI onto existing workflows — which McKinsey calls “setting bad processes in concrete.”

“The business value of AI will correlate less with how much you spend on AI models, and more on how well organisations redesign everyday workflows that see AI used in controlled environments with verifiable actions and hard guardrails.”

— McKinsey, AI’s Next Act

3. Active Leadership, Not Passive Sponsorship

Bain’s research in life sciences reveals a pattern applicable across industries: insufficient C-suite sponsorship is the top reason companies feel stuck in early AI adoption. Passive support isn’t enough. Executives at successful companies regularly review AI initiatives using measurable KPIs, hold initiative leaders accountable, and clear roadblocks.6

“The best companies will explicitly link AI to enterprise strategy, executive accountability, disciplined capital allocation, and centralized governance.”

— Bain, In Life Sciences AI Moves Fast When Leaders Do

4. Workforce Investment Over Technology Procurement

BCG’s data shows Trailblazer CEOs allocate 60% of AI budgets to workforce upskilling — compared to 27% and 24% for Pragmatists and Followers respectively.1 The leaders treat AI as a capability-building exercise, not a vendor relationship.

EY notes a significant mindset shift: the proportion of CEOs expecting AI to reduce headcount dropped from 46% in January 2025 to 24% in December 2025. Instead, 69% now believe AI investments will maintain or increase employment.7

The Emma Grede Framework

Perhaps the most practical mental model came from Emma Grede (Good American, SKIMS) at NRF 2026. PwC highlights her “second executive brain” approach:

“I think the question that I ask myself most is, is this something I should be doing? Is this something my team should be doing? Or should AI be doing it? AI can do certain things at the speed that no human would ever find manageable. So for me, it’s not about taking anything human out of what we do. It’s actually leaving ourselves the time to do the stuff that only we can do.”

— Emma Grede, via PwC NRF 2026 Report

This three-way sort — me, my team, or AI — offers a daily operating framework that cuts through the hype. The question isn’t “where can we use AI?” but “what should each capability be doing?”

Industries Most at Risk

BCG and Moloco’s Consumer AI Disruption Index surveyed 238 senior marketing leaders. The finding: 67% expect high AI-driven disruption to their vertical’s consumer journey.8

| Most Vulnerable | Most Resilient |

|---|---|

| News | Auto Manufacturing |

| Travel | FinTech |

| Auto Marketplaces | Financial Services |

| Retail | Media/Streaming |

The underlying pattern: industries where AI can intermediate customer relationships — finding products, comparing options, making recommendations — face the highest disruption. Industries with physical moats or regulatory complexity have more time.

The Consensus View

Synthesizing across all six firms, the January 2026 message is clear:

- Investment isn’t the differentiator. Everyone is investing. The gap is between those who transform and those who merely spend.

- CEOs must personally own AI strategy. Delegation to IT isn’t working. The leaders are upskilling themselves and taking direct accountability.

- Foundations matter more than ambition. Companies with strong data, governance, and technology environments are 3x more likely to see returns.

- Agentic AI is coming fast — governance isn’t. 85% plan agents, 21% have governance. This is the next failure point.

- Process redesign beats tool deployment. Only 30% are redesigning work. The rest are automating broken processes.

- 2026 is the audit moment. The gap between leaders and laggards is becoming structural, not temporary.

McKinsey captures it precisely:

“Competitive advantage will depend on a sustained investment in fundamentals rather than incremental experimentation. Organisations that hard-wire AI into redesigned processes, build confidence through robust governance and controls, and invest in the human and technical foundations will be better positioned to translate AI capabilities into performance gains.”

— McKinsey, AI’s Next Act

The Question for Your Board

The consulting firms agree: the question is no longer “Are we investing in AI?” Everyone is.

The question is: “Are we investing in the transformation that makes AI investment matter?”

Based on this synthesis, the board-level conversation should address:

- Are we in the 12% seeing dual benefits, or the 56% seeing none?

- Is AI owned by the CEO or delegated to IT?

- Are we redesigning processes or bolting AI onto broken workflows?

- What governance do we have for autonomous agents?

- How much of our AI budget goes to workforce capability vs. technology procurement?

2026 is the year the gap becomes structural. The consulting firms are aligned: the window is closing.

References

- BCG. “As AI Investments Surge, CEOs Take the Lead.” January 15, 2026. bcg.com/press/15january2026-as-ai-investments-surge-ceos-take-lead

- PwC. “2026 Global CEO Survey.” January 19, 2026. pwc.com/gx/en/news-room/press-releases/2026/pwc-2026-global-ceo-survey.html

- Deloitte. “State of AI in the Enterprise 2026.” January 21, 2026. deloitte.com/us/en/about/press-room/state-of-ai-report-2026.html

- McKinsey. “AI’s Next Act: McKinsey AI Leaders on the Year Ahead.” January 16, 2026. mckinsey.com/uk/our-insights/uk-insights/ais-next-act-mckinsey-ai-leaders-on-the-year-ahead

- Bain & Company. “Reimagining Merchandising in the Era of Agentic AI.” January 2026. bain.com/insights/reimagining-merchandising-in-the-era-of-agentic-ai/

- Bain & Company. “In Life Sciences, AI Moves Fast When Leaders Do.” January 2026. bain.com/insights/life-sciences-ai-moves-fast-when-leaders-do-snap-chart/

- EY. “CEOs Double Down on AI, Transformation and M&A to Drive Growth.” January 20, 2026. ey.com/en_gl/newsroom/2026/01/ceos-double-down-on-ai-transformation-and-m-and-a-to-drive-growth-amid-uncertainty-in-the-global-economy

- BCG and Moloco. “Consumer AI Disruption Index.” January 21, 2026. bcg.com/press/21january2026-marketing-leaders-expect-ai-driven-disruption-consumer-behavior

Discover more from Leverage AI for your business

Subscribe to get the latest posts sent to your email.